![]() Trade capture

Trade capture

All valid trades/positions are included in the risk calculation.

1. Count is matching - No trade/position is missing or added

2. Economic aspect factors are captured correctly

3. Reporting factors Position amount is correct![]() Market data is correct and complete

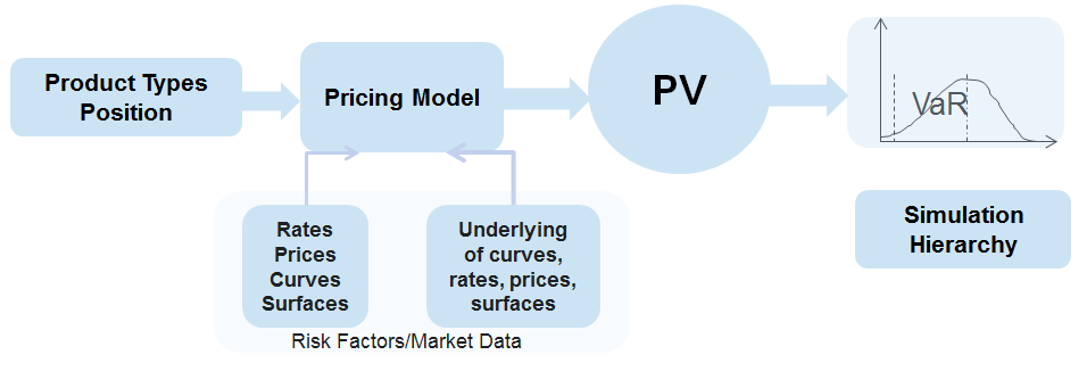

Market data is correct and complete

1. IR Curve, CDS, and underlying securities

2. Vol surface/Cube

3. Closing rate/price![]() Risk Metrics

Risk Metrics

1. Delta, Gamma

2. Vega

3. MTM/PV![]() Daily VaR measures

Daily VaR measures

1. DGV VaR

2. Stress VaR

3. Full Reval VaR![]() Stress VaR

Stress VaR![]() Back test

Back test![]() Stress test

Stress test![]() Breach investigation

Breach investigation![]() Limit Letter monitoring

Limit Letter monitoring

Testing Portfolio Section- Data Sampling

Cover major product types, as such the pricing models

Cover major product types, as such the pricing models

Cover most used curves in the pricing as such the most frequently used market data and risk factors

Cover linear and nonlinear products

Cover the trading and corresponding hedging portfolios

Cover trades with variety of maturities

Cover EQ, IR, FX, CO asset classes